Why this exists

I wanted to better understand the AI value chain and which companies have the biggest roles to play going forward.

NVIDIA is the obvious answer, but it is not the whole answer. The interesting part is everything underneath it: power, grid work, construction, cooling, memory, packaging, optics, cloud capacity, and the companies that become important before most people are paying attention.

What it does

The atlas breaks the AI buildout into a set of research artifacts:

- A fifteen-layer map of the value chain, from commodities and power through silicon, networking, cloud, and applications

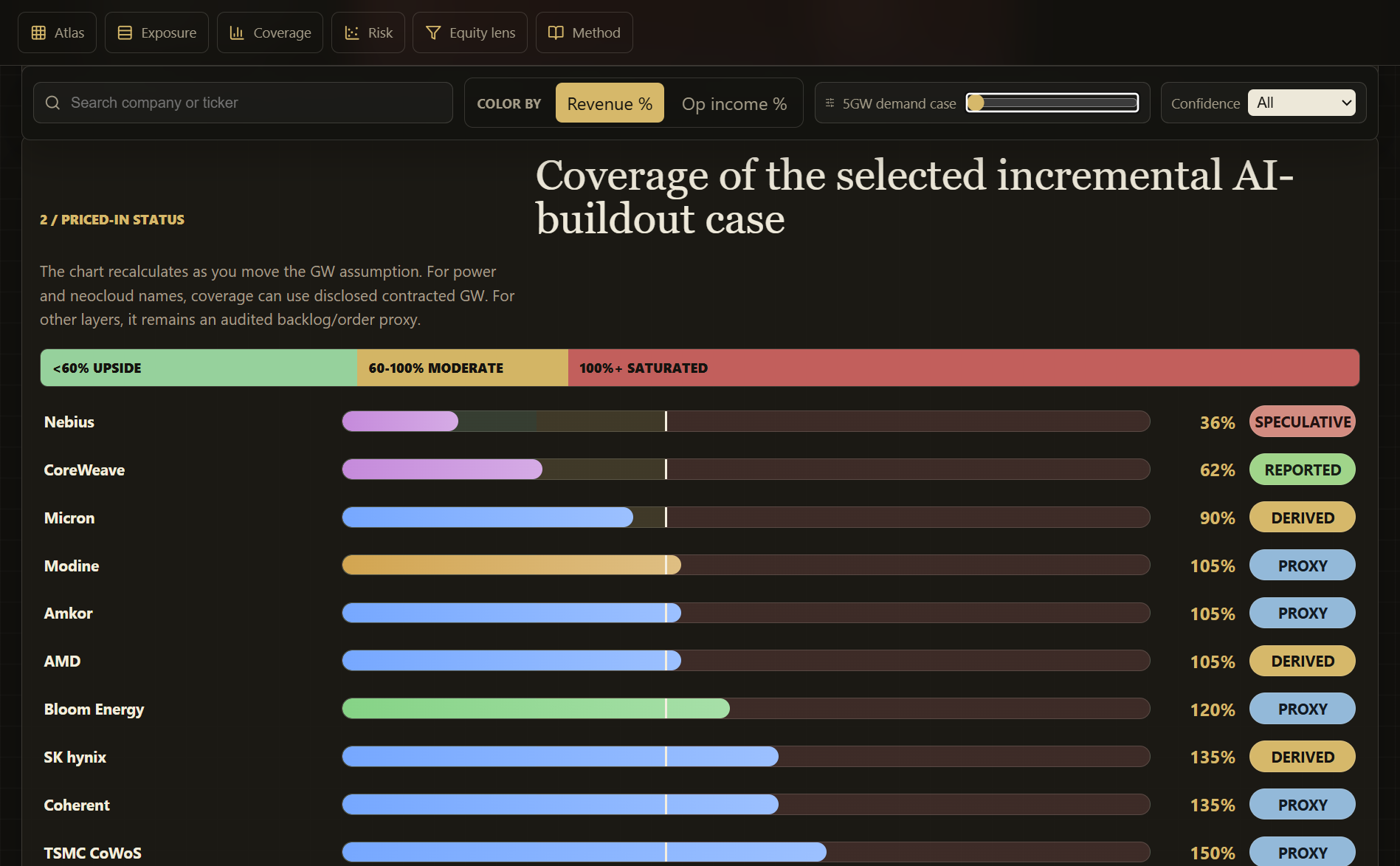

- A coverage chart that changes when the assumed incremental AI power demand changes

- A coverage-versus-substitution-risk view for finding bottlenecks

- A public equity lens for names worth deeper underwriting

- A company drawer with thesis notes, audit notes, source logic, and links back to primary-source anchors

The point is not to pretend the numbers are perfect. It is to make the assumptions visible enough to pressure-test.

How it works

- Map the chain: The app starts with fifteen layers, from commodities and grid equipment through accelerators, networking, hyperscalers, and neoclouds.

- Score the companies: Each company gets estimated AI revenue mix, operating-income mix, layer share, coverage, substitution risk, and confidence level.

- Show the bottlenecks: The UI turns those estimates into exposure blocks, coverage bars, a risk scatter, and a shortlist of public names.

- Change the demand case: The slider lets the same dataset answer a different question if the AI buildout is bigger or smaller than the base case.

- Show the receipts: Detail drawers link claims back to source IDs and audit notes, with proxy and speculative assumptions labeled instead of hidden.

What’s next

- Go deeper on scalability. If demand takes off like the bulls think it will, the next question is who can actually ramp production in months or a few years.

- Separate importance from capacity. A company can be crucial to the value chain and still be flat-footed if the demand curve gets too steep.

- Replace proxies with better evidence. More filings, backlog data, capex plans, and capacity disclosures should replace every rough estimate over time.

What I learned

I knew NVIDIA was central. I had not really internalized how many less obvious companies are driving the value chain around it.

Quanta Services is a good example. It is not the first name most people think of when they think “AI,” but the buildout does not happen without the boring physical work: grid connections, power equipment, construction, cooling, and capacity actually getting built.

Status

Shipped. Running on Cloudflare Workers, with GitHub Actions deploying every push to main.